Some History

1935: Social Security initiated, declared tax free.

Originally, Social Security benefits were not taxable income. This

was not, however, a provision of the law, nor anything that

President Roosevelt did or could have "promised." It was the result

of a series of administrative rulings issued by the Treasury

Department in the early years of the program.

1974: Employee Retirement Income Security Act created the IRA.

Money could be deposited into this account originally by an

individual, then changed to married couples. The deposits would

then have to be deducted from your income on your annual tax return.

This account is now referred to as your Traditional IRA.

1979: IRS added section 401 subsection K to their Internal Code.

Deposits into your 401K are made directly by your employer and are

already calculated into your W2 form. Employees can made direct

pre-tax contributions and their Employer has the right to add

matching funds.

1983: Social Security Act Amendment, 50% taxable.

Congress agreed on a bi-partisan level to recognize that the FICA

contributions by employees were made after tax, but the matching

contributions by the employer were tax deductible. They decided

that, as the employer�s half of our Social Security benefits were

returned to us, they should be taxable income.

They devised a formula for the "basis" of the taxation of our

benefits to be the employers half of the benefits we receive

plus our other taxable income. Being the Government, they also

include decided to include thing like our tax free income from

municipal bonds, etc. They set the "basis" starting points for

the 50% taxation of our benefits at $25,000 for single individuals

and $32,000 for married couples.

Using the 2019 Social Security inflation factor for 1983 income

of 3.3, those limits would be $83,500 and $105,600 in 2019 dollars!

All of our representative took the opportunity to let the press

know that they were "only taxing the rich". Unfortunately, they

"forgot" to include COLA adjustments on those limits and the taxation

still starts at $25,000 and $32,000 today!

For every dollar that your "basis" exceeds your starting point, 50

cents of your benefit becomes taxable income until 50% of your total

benefit has become taxable income.

1993: Omnibus Budget Reconciliation Act, 85% taxable.

Congress now realized that the total we were getting back as Social

Security benefits was far greater than our original contributions

and decided to add a second layer of taxation at the 85% level.

They agreed on the second level starting points of $34,000 for

individuals and $44,000 for married couples.

Every dollar that your basis exceeds this second level would change

your dollar for dollar taxation from 50 cents to 85 cents until 85%

of your total benefit has become taxable income.

1997: Taxpayer Relief Act, Roth IRA established.

I�m not sure if Congress was taking pity on us, or they just wanted

their tax dollars sooner than later, but you can put already taxed

dollars into your Roth IRA account and then remove your contributions

and any growth within the account tax free during your retirement

years.

This also allows us to perform Roth Conversions. You can move funds

from your taxable Traditional IRA account to your Roth IRA account

as long as you pay the taxes on the converted amount as if it were

normal income.

Your only limitation is that you have to wait at least five year from

the date you created your Roth account before you can make any

withdrawals.

The Shift from Pensions to 401Ks

The concept of retirement has changed drastically over the past 45 years.

Retirement for our parents relied on their Social Security income and their

Pensions.

A pension was basically a Lifetime Contract. You received a

fixed monthly income for the rest of your life, and some pensions also

included cost of living increases!

Pensions today are being replaced by 401Ks and IRAs. These are merely

different methods of saving money for retirement. There is NO CONTRACT

and when the money runs out, the income stops, and stock market volatility

and taxes can play significant roles in how long our savings will last.

Longevity is becoming a major factor in our retirement. Will you outlive

your money?

- Eliminating costly taxes

- Minimizing your stock market risk

- Guaranteed income for life

This lack of Guaranteed Lifetime Income has resulted in a significant shift

in the age when many of us are starting our Social Security Benefits.

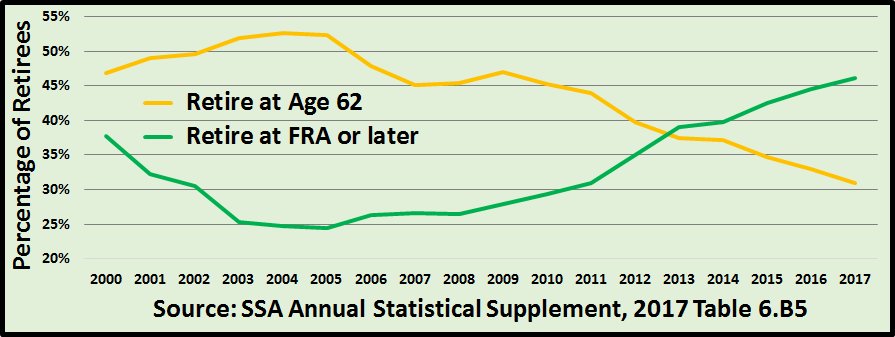

The 2004 Social Security Statistics indicated that 53.65% of all Americans

started their benefit at age 62 while only 24.75% had reached their Full

Retirement Age or older. The 2017 statistics now show that only 30.9% are

starting their benefits at age 62 while 46.2% are waiting until their full

retirement age or later.

As pensions are being replaced by individual savings, the only source for

guaranteed lifetime is becoming our Social Security benefits. Many of us

are beginning to realize that starting our benefit at the lowest possible

guaranteed income level at the earliest possible age is not the best strategy

to insure a livable income for the remainder of our lives.

|