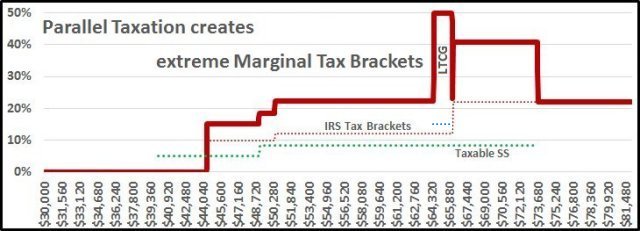

The Marriage Penalty

Using the spreadsheet supplied with this website, here is an example of the marginal

tax hump for a single individual with a $30,000 Social Security benefit. This

individual can also have an extra $34,567 of pre-hump taxable income,

resulting in a 2018 after

Federal tax net income of $60,115, a 6.9% overall tax rate. Their next $9,138 will

be taxed at 40.7%. If two single individuals were living together as domestic

partners, their combined income and taxes would merely be twice the size of each

individual. Their pre-tax hump net income would be $120,230.

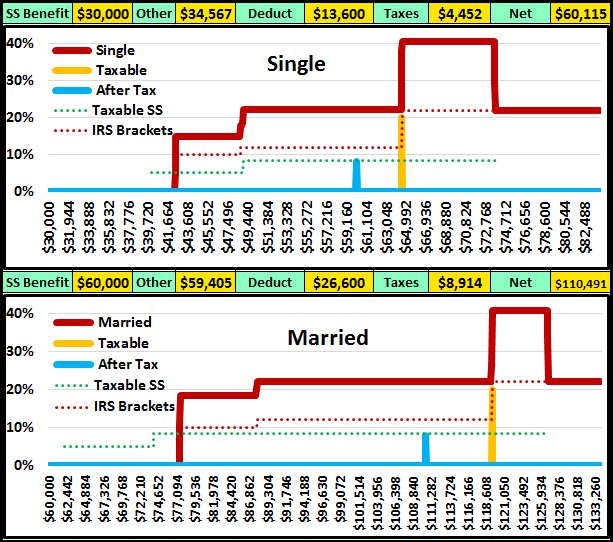

The second image representing the marginal tax hump faced by the same couple

if they decided to get married and file a joint return.

Note how the dotted green Taxable SS line starts well before the start of their

taxation. The SS taxation of each individual in the first graph starts at a Basis

Income level of $25,000, a combined $50,000 for the domestic partners, while taxation

for the married couple starts at only $32,000. This earlier start of SS taxation

results in a pre-hump net income of only $110,491 for the married couple, a

Marriage Penalty of almost $10,000.

What Causes The Marriage Penalty?

The primary cause of the Marriage Penalty is the starting positions for the taxability

of your Social Security benefits. The calculation of the "basis" for this taxation

is the same, basically half of your Social Security benefits plus your other taxable

income. 50% taxability starts when the basis exceeds $25,000 for a single individual,

which would double to $50,000 for domestic partners. But the 50% taxability

starts at only $32,000 for a married couple, and 85% taxability starts at $44,000,

which is still $6,000 less than the $50,000 combined start of the 50% taxability

level for the domestic partners.

At the $50,000 taxable basis level $11,100 of the married couple’s Social Security

is being taxed while none of the domestic partner’s benefits are taxable. Over the

next $18,000 of income another $15,300 of the married couple’s benefits become taxable

while only $9,000 of the domestic partner’s benefits become taxable. At this point

the marriage penalty reaches its maximum where an additional $17,400 of the married

couple’s benefits are being taxed.

This $17,400 taxable penalty continues for variable amount of income based on the

size of the Social Security benefits levels. If the total benefit levels of each

couple are identical, the domestic couple will continue to increase their taxable

benefits for another $20,471.

So, basically, the married couple’s Social Security benefits are taxed at lower

income levels. Their potential tax free income is $7,427 less, and their personal tax

hump starts $9,731 before that of the domestic partners. Since this results in them

saving less tax dollars at the lower income levels, the size of their personal hump

is also smaller because they have less to give back to the IRS.

At higher income levels, when everyone is paying their full hump taxes, everything

basically evens out because at that point everyone is paying taxes on the same 85% of

their Social Security Benefits. Married couples just pay it earlier. The only penalty

that remains is that the additional over 65 standard deduction is only $1,300 for

married individuals and $1,600 when you are single.

The Widow(er) Penalty

If you did not plan your inheritance properly, your surviving spouse could have

the same income as you did as a married couple while being faced with higher tax rates

because they will have to file the same income levels as a single individual instead

of a married couple.

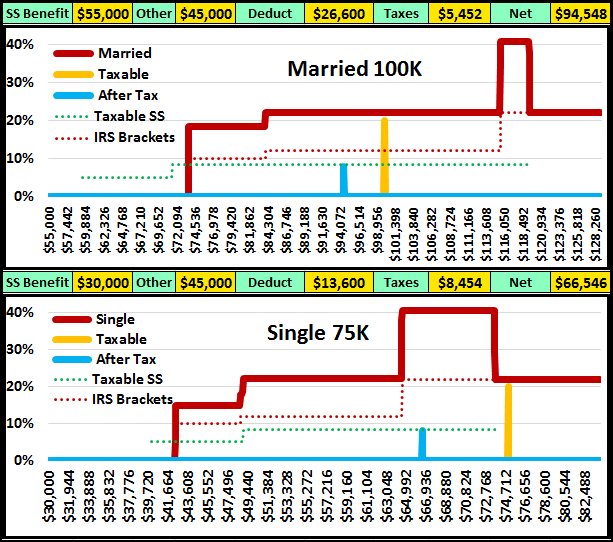

In this example we see a married couple with $25,000 and $30,000 Social Security

benefits plus additional taxable income of $45,000 from pensions, annuities, IRA

withdrawals, etc. Their total annual married income is $100,000 and the top graph

shows that their income level is more than $15,000 below their personal 40.7% Marginal

Tax Hump. Their federal taxes will be $5,452.

When one of them passes away, the survivor will lose the $25,000 SSB and keep the

larger SSB. Assuming that all of their pensions, annuities and other income continues

for the survivor, the additional income will remain at $45,000. The Widow’s annual

income will drop to $75,000 and the lower graph shows that her income level will

be higher than the top end of her personal 40.7% tax hump created as a single individual

vs. a married couple. Her federal taxes will be $8,454!

The Widow is not only losing the $25,000 SSB, but also has to pay an additional

$3,002 in taxes!

Can this be avoided?

One of the things they might have considered would be to calculate their taxes in

December each year, then do a Roth Conversion that will maximize their 22.2% Marginal

Federal Tax Bracket. If the widow could reduce her other taxable income by $11,000

each year she would save $4,130 in taxes. This could be done with an annual withdraw

from a tax free Roth account of $6,870 ($11,000 minus $4,130).

If your inheritance to each other passes as taxable income the immediate and lifelong

tax penalties could be substantial. Even if the taxes are not immediate as your

individual IRA is combined, sort of tax free now, with your spouses IRA, the larger

combined IRA will have a much larger MRD, Minimum Required Distribution, for the

remainder of the surviving spouses lifetime.

|