Social Security / Retirement To Do List

Before Retirement

- The first item on the list is very obvious, start planning early!

- There are far too many individuals in their 50s with less than $25,000

saved for retirement!

- At work make sure that you are contributing whatever is necessary to get your

full company match.

- You can’t beat a 100% return on your savings!

- Make sure that you open your Roth account by at least age 55.

- There is a 10% penalty if you withdraw money from your Roth within 5

years of the date you opened the account.

- Create your "My Social Security" account as soon as possible.

- Get your PIA (primary insurance amount) each year and do the

calculations to see if you will have a personal tax hump if you retire

at your normal retirement age.

- Check your mortgage!

- If the extra after tax money necessary to make your mortgage payments

is going to push you into your Tax Hump, look for ways to pay off your

mortgage before starting Social Security.

After Retirement

- Check your anticipated tax status during the year.

- You are trying to keep on track so you can avoid your personal tax

hump.

- Make your final tax status check close to the end of the year.

- Try to maximize your pre-hump withdrawals from your IRA.

- Build up non-IRA savings

- Reduce the size of your MRD, Minimum Required Distribution, after age 70.

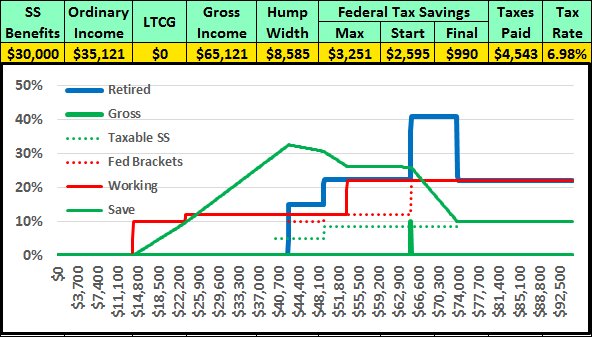

Here is an example of what pre-planning can do for you. Let’s say that you need

$1,000 to pay a bill. We know that the Marginal tax rate before the Tax Hump is

22.2% and 40.7% after you are in The Hump.

- You will need to withdraw $1,285.35 from your IRA and pay 22.2%, $285.35, in

the pre-hump 22.2% marginal tax bracket to end up with the $1,000 you need

after tax.

- If you are in The Hump you will need to withdraw $1,686.34 from your IRA and

pay 40.7%, $686.34, in the 40.7% Marginal Tax Hump to end up with the same

$1,000 that you need after tax.

- Pre-planning around your personal Tax Hump could save you $400.99 for

every extra $1,000 that you need to spend!

- If your personal tax hump starts with the 49.95% marginal tax rate created by

LTCGs, you will need to withdraw $1,998 from your IRA, and pay 49.95%, $998

to end up with the $1,000 that you need after tax.

- Your pre-planning savings would jump to $712.65 for every extra $1,000

that you need to spend!

|