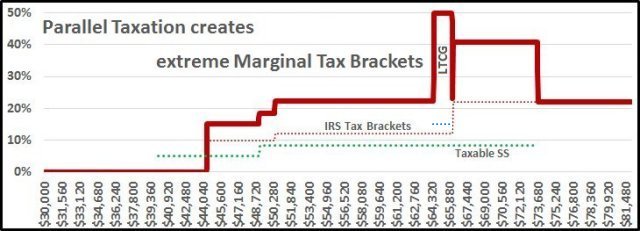

The graph at the top of this page represents the Marginal Tax Brackets faced

by a retired individual, over 65, with a $30,000 annual Social Security benefit,

and $3,000 in Long Term Capital Gains. This graph could be divided into 4 logical

sections:

The individual is paying ZERO taxes on about their first

$44,300$44,567 of gross

income because Social Security benefits and Long Term Gains are "tax

deferred" income.

Over the next $20,100 their marginal tax rates are similar to the 10%, 12%,

and 22% standard tax brackets that we are all used to before retirement.

Their actual "marginal tax rates" created by what we call "Parallel

Taxation" will be 15%, 18.5%, and 22.2%. The overall tax rate over more

than their first $64,000 of gross income will be less than 7.5%.

Then comes the problem that we will discuss in great detail on this website,

the "Tax Hump". Over the next $9,100, from about $64,500 to $73,600 of

gross income, they will pay marginal tax rates of 49.95% and 40.7%. The

overall taxes paid during this income range will be $3,841 for an average tax

rate of 42.21%, more than 5% higher than the maximum Federal bracket of 37%

paid by millionaires and billionaires!

After their gross income reaches about $73,700, their "Parallel

Taxation" ends and their tax rates will return back to "normal", 22%,

24%, etc.

Don’t let this Tax Hump scare you. Its location and size is based

on the amount of ZERO tax income you can create. So, do what you can to make it as

large and scary as possible, just be aware that it is there and also do what you can

to make sure that your retirement income sources will keep you in sections A and B

while you enjoy the retirement lifestyle that you have been dreaming about.

Disclaimer

I am not a qualified Investment Advisor or Tax Accountant or CPA. I am totally

unqualified to give you any of this advice. So, use the information in this

presentation at your own risk! The problem here is that no one else will give

you this information.

If you ask your broker or investment advisor about the marginal tax rates you pay

while receiving Social Security, they will tell you to talk to your tax accountant.

They can literally lose their brokers license if they give you tax advice!

Your tax accountant at H&R Block or other storefront tax services rarely have any

idea which are the best investment strategies to use or which stocks, bonds, or funds

to invest in.

A CPA can give you this advice, but let's be honest, is it worth their time and

effort to help you save maybe 1, 2 or 3 thousand dollars a year? How much are you

willing to pay for the time necessary to provide that service? I talked to the

investment guy at my bank and that is exactly what he told me.

A quick overview!

July 22, 2018: The Bureau of Labor Statistics says that the average household led

by a retiree, over 65, makes $48,000 annually before taxes. The highest Federal

Tax Bracket for someone making over $500,000 is 37%.

If you are retired and single with a gross income of $46,200 or married

with a gross income of $86,700, your "Marginal Tax Rate" as your income and your

Social Security Benefits are being taxed at the same time could be as high as 40.7%

and if you also have Long Term Capital Gains from your investments that marginal

rate could be 49.95%.

These marginal rates are real. The remainder of this article and the accompanying

Excel spreadsheet will help you to find out if your personal income sources during

retirement will expose you to these extreme rates and help you find ways around

them if possible.

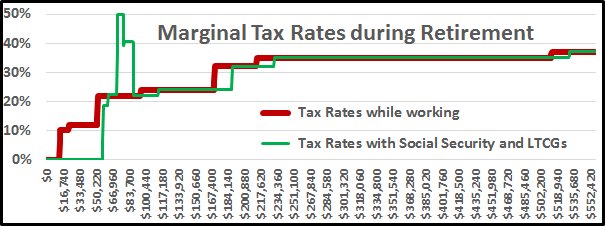

This graph illustrates the situation perfectly. The green line in this graph starts

at a significantly higher gross income level than the red line. You are initially

saving a considerable amount of tax dollars because your Social Security benefits

and Long Term Gains are "tax deferred". They are not "tax free", and as your other

income increases the government forces you to return most of those tax savings. It

is not difficult to see the "Tax Hump" that occurs while the IRS starts taxing your

Long Term Gains and slowly makes 85% of your Social Security benefits taxable income.

The tiny gaps on the remainder of the graph

show where 15% of your Social Security benefits continue to be tax free.

Social Security started in 1935 and the benefits were expressly

excluded from federal income taxation under Treasury Department

Tax Rulings. This all changed with the 1983 amendments to the

Social Security Act. A typically complex government formula was

created to define the basis for the taxability of your benefits.

The "basis" for taxation is one half of your Social Security

benefits plus your other taxable income. This is the Government,

so other taxable income includes "tax deferred" Long Term Capital

Gains, municipal bond interest, and a few other things. Income

from a Roth account is NOT included!

Beginning in 1983 if your basis income exceeded $25,000 for an

individual or $32,000 for a married couple filing jointly up to

50% of your SS benefit was subject to your marginal tax rate.

So for the first time in history SS benefits became subject to

taxes.

The 1993 Omnibus Budget Reconciliation Act (the OBRA) contained

a provision that altered this rule and created a second threshold

that would subject up to 85% of your SS benefit to taxation if

your basis income exceeds $34,000 for an individual or $44,000

for a married couple filing jointly.

One thing to note is that these thresholds are not indexed for

inflation. They are still the same amounts as when they started

in 1983 and 1993. This has the effect of capturing more and more

people within the taxation net each year. In 1983 less than 10%

of all benefit recipients were subjected to taxes on benefits,

but currently that number is over 30% and will continue to rise.

Marginal Tax Brackets

Federal Bracket

Taxable at 50%

Taxable at 85%

LTCGs at 15%

As each additional dollar of income causes

50 cents or 85 cents of your Social Security Benefits to also become taxable

income, your taxable income increases by $1.50 or $1.85, not just one dollar,

which creates the following marginal tax brackets.

10%

15%

18.5%

12%

18%

22.2%

49.95%

22%

N/A

40.7%

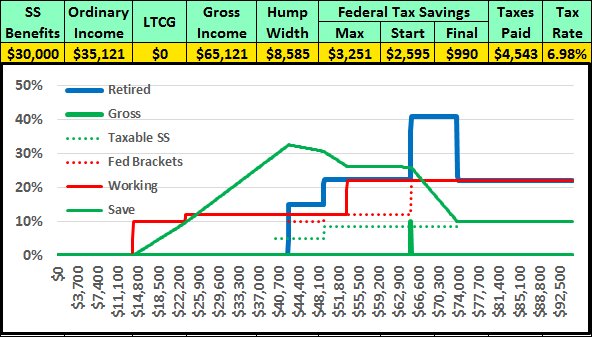

Let's zoom in on the problem!

During retirement, everyone has their own "Personal Tax Brackets" and their own

"Personal Tax Hump". Click on the radio buttons below to see how the size and

shape of your personal hump will depend on the size of your personal Social

Security Benefit level, your marital status, and your other sources of

retirement income.

This interactive image is based on the 2019 tax brackets!

The red "Working" line is relatively constant in each image with the

exception of the effect of Long Term Capital Gains. Note how the blue line

changes as you click the various radio buttons in the form above the image. Also

take note of how the size and shape of the green tax "Save" line changes in

conjunction with the changes to the blue "Retired" Marginal Tax Rate line.

Note that the gross income scale at the bottom of each graph exactly doubles when

you click the Married radio button. This allows the graph to properly represent

the Marginal Tax Rates per person. Also note how the dotted green Taxable SS line

shifts to the left for married couples which represents the marriage penalty where

the married couple start paying taxes on their benefits at $32,000, $16,000 per

person, vs $25,000 for a single individual.

Note how the blue line changes when you click the LTCG radio button. Each blue line

starts later because the LTCG is tax deferred. The position and width of the tax hump

remains relatively constant except that it now starts at the 49.95% Marginal Rate

before dropping back to 40.7%.

Our Audience!

The value of this presentation depends on your filing status, the size of your

personal Social Security benefits and the cost of the lifestyle you want to live

while retired.

Single

Tax Free

After 2018 Taxes

Your Personal Tax Hump

SSB

Pre-Hump

Tax Rate

Start

End

Width

$20,000

$33,600

$52,411

8.50%

$56,865

$58,706

$1,841

$30,000

$42,400

$60,114

7.41%

$64,568

$73,706

$9,138

$35,000

$46,569

$63,910

6.97%

$68,364

$81,205

$12,841

$40,000

$50,733

$67,816

6.57%

$72,270

$88,706

$16,436

Married

Tax Free

After 2018 Taxes

Your Personal Tax Hump

SSB

Pre-Hump

Tax Rate

Start

End

Width

$50,000

$69,865

$102,795

8.66%

$111,702

$111,941

$239

$60,000

$77,568

$110,498

8.06%

$119,405

$126,941

$7,536

$70,000

$85,271

$118,201

7.54%

$127,108

$141,941

$14,833

$80,000

$92,973

$125,904

7.07%

$134,811

$156,941

$22,130

Single

Tax Free

After 2019 Taxes

Your Personal Tax Hump

SSB

Pre-Hump

Tax Rate

Start

End

Width

$20,000

$33,850

$52,876

8.59%

$57,419

$58,706

$1,287

$30,000

$42,567

$60,579

7.50%

$65,122

$73,706

$8,584

$35,000

$46,734

$64,430

7.05%

$68,973

$81,205

$12,232

$40,000

$50,900

$68,281

6.65%

$72,824

$88,706

$15,882

Married

Tax Free

After 2019 Taxes

Your Personal Tax Hump

SSB

Pre-Hump

Tax Rate

Start

End

Width

$52,000

$71,622

$105,211

8.64%

$114,297

$114,940

$643

$60,000

$77,784

$111,373

8.16%

$120,459

$126,941

$6,482

$70,000

$85,487

$119,076

7.63%

$128,162

$141,941

$13,779

$80,000

$93,190

$126,779

7.17%

$135,865

$156,941

$21,076

The 2017 statistics released by the Social Security Administration show a significant

shift from 2004 when the majority of recipients starting their benefits at age 62

to the 2017 stats that show only 30.9% starting at age 62 while 46.2% are now waiting

at least until their Full Retirement Age.

If you are still among those who are starting your benefits as early as possible and

are willing to get the smallest possible benefit for the rest of your life; then your

personal SSB will be so low that the Width of Your Personal

Tax Hump will be extremely narrow or does not even exist, then this site will

be of little or no value to you. Every $100 you can eliminate from your personal

hump will only save you $18.70 in Federal taxes. If your personal tax hump is only

$200 wide, is it worth the effort necessary to save less than $40 a year?

A special note here! Yes it is true that higher Social Security benefits create

larger tax humps, but they also give you the opportunity for more Tax Free

income. Also take note that the Start of Your Personal Tax Hump is the

start of your 22% Federal tax bracket. The total Federal taxes due at the Start

of Your Personal Tax Hump if you are single is only

$4,453.50 and only $8,907$4,543 and only $9,086

if you are married.

Could you live comfortably on your After Tax, Pre-Hump, income level

while paying a very small Federal Tax Rate? With proper pre-planning for

your retirement, you could also supplement this income level with additional tax

free cash from sources like a Roth account!

If your desired lifestyle puts your taxable gross income well above the End

of Your Personal Tax Hump, the amount of effort that will be required to

eliminate your extreme Marginal Tax Rates might be overwhelming. But, if the

expected Width could be large and you can live comfortably on a gross

taxable income near the Start of Your Personal Tax Hump, maybe enhanced

with some tax free income from a Roth or other sources, the information in this site

could be very valuable to you. Again, as you should do with all financial advice,

double check this information with other sources.

Do not rely on these estimates, contact Social Security to get your actual numbers! These

are rough estimates of your annual benefits based on your average inflation adjusted income

over the top 35 years of employment based on Social Security’s on-line social estimation

form.

In 2018 your Social Security benefit level will be 90% of the first

$10,740, plus 32% of the next $54,024, plus 15%In 2019 your Social Security benefit level will be 90% of the first

$11,112, plus 32% of the next $55,884, plus 15%

of your remaining average inflation adjusted income.

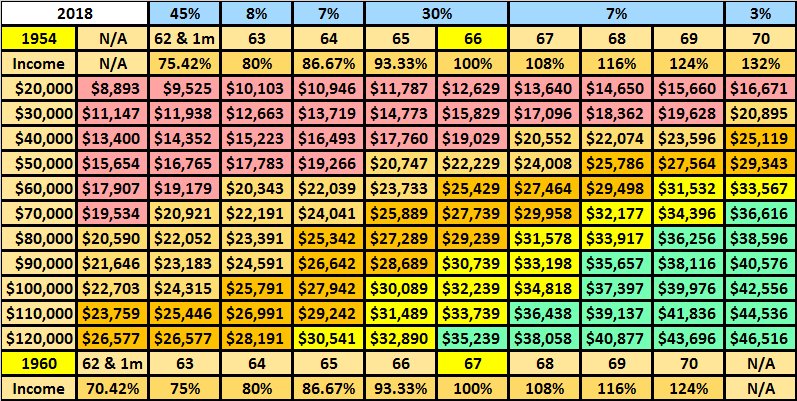

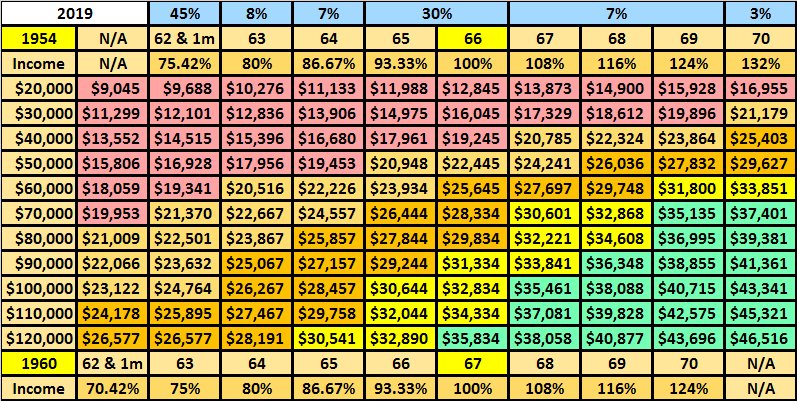

The top blue two lines shows the percentage of individuals who start their benefits

at various ages. The top line indicates which column to use based on your retirement age if

you were born before 1954. The bottom two lines show the same information if you were born

after 1960.

We are providing an Excel spreadsheet that you can use to determine if you have a

marginal Tax Hump, how large your personal hump is, and help you find ways to avoid it.

The spreadsheet is on our personal google drive. Our spreadsheet is less that 1 MB and

according to google every file which is less than 100 MB is scanned for viruses. This

is the best we can do to make sure that what we are giving you is virus free, but

download and use it at your own risk!

Our Social Security benefits are "tax deferred". We get them tax free, then as our

income increases, the benefits slowly become taxable until 85% of our benefits have

been taxed. The "Marriage Penalty" is that a married couple's benefits are taxed at

lower income levels then single individuals!

There are a lot of web conversations that say if you start your Social Security

at age 66 vs age 62, you will not Break Even until age 77 or 78. Based on the way

they do their calculations these number are correct and real, but they do

not represent reality! Their calculation are based on the Gross amount of

Social Security benefit that you are getting from the Government.

The reality is that we do not live on our gross incomes, we live on our net, after

tax, incomes. Getting less "tax deferred" income means that you will need more "taxable"

income to reach the same after tax desired standard of living. When you redo the

Break Even calculation using net income, the Social Security benefit you are getting

from the Government minus the Federal Taxes you are giving back to the

Government, your Break Even age drops to 73, and if the tax hump is involved, even

as low as 71.

Roth contributions and conversions are a good way to avoid your Tax Hump if you do

them early enough. There is a 10% penalty if your withdraw money from a Roth within

the first 5 years of opening the account.

As a survivor, you probably have to plan for retirement twice, once for your

survivor benefits and again for your own. It is far easier for a surviving spouse to

wait for a much higher final Social Security benefit. This will make it easier for

them to reach

a retirement "Sweet Spot" where their after

Federal tax income levels could reach $50,000 to $65,000 or more with overall Federal

Tax Rates of considerably less than 10%.

Minimum Required Distributions (MRD) from your IRA and 401K accounts start at the

age of 70. These distributions can push you into your personal Tax Hump unless you

have planned for them.

The income levels when the taxation of your Social Security benefits are not COLA

adjusted, so the percentage of American effected by this taxation and The Tax Hump

is increasing each year.

This Social Security form shows you how your full retirement age benefits

are calculated. Take special note of the "Index factors" that are used to

adjust each year’s earnings for inflation before choosing the 35 years with

the highest amounts to calculate your benefit level.